03.05.2022

Im Fokus: US-Staatsanleihen-Renditekurve sendet gemischte Signale | Mai 2022

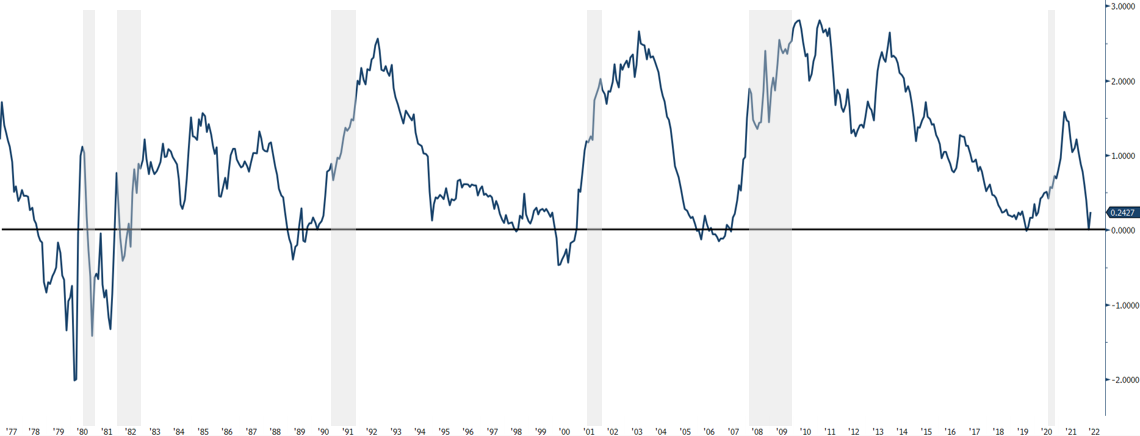

In the early days of the month of April, the closely watched 2Y/10Y yield curve has inverted multiple times over a short time span. High emphasis is put on this point of data as it has in the past often been synonymous in announcing a recession of the US economy. While many strategists explained that the rise in concern over this matter should not spark fear in the markets, others highlight putting the 2Y/10Y in correlation with the Consumer Optimism Gap clearly illustrates that a downward slopping yield curve matches a fall in consumer optimism and eventually provides fertile ground for a recession.

US 2Y/10Y - Average of 18 months from inversion to recession:

History tells us since the 1960s’ every recession where economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters has only occurred after an inversion of the 2Y/10Y. Following this chain of thought, we can now suppose that additional risk is weighing in the basket in seeing a declining growth of the US economy in one to two years time following the rise of the 4th of May.

US 2Y/10Y vs Consumer Optimism Gap:

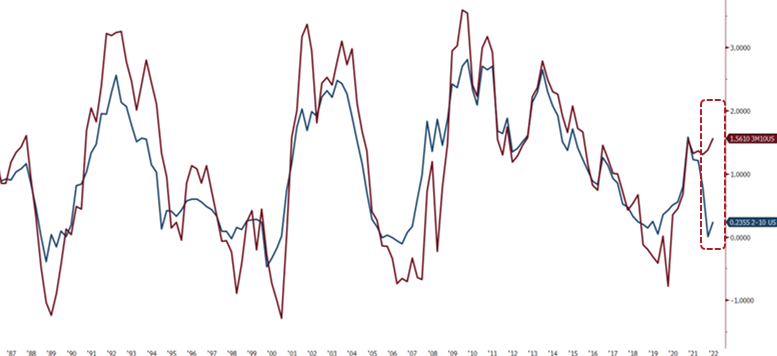

Don’t panic the 3M/10Y still remains steep

All yield curves between 2 and 10 years have inverted. Remains the 3 month, which is taking a steep route in positive territory. This phenomenon can be interpreted in two ways. The first could be a reflection of the FED being behind the curve. Something that should not last over the upcoming quarters as future hikes are on target.

An upward slopping curve happens when investors require additional return on debt as they envision greater default risk of the underlying or a possible fear of inflation. The divergence between the 3M/10Y could also be a signal of increasing hawkishness from the FED in the upcoming years.

Finally, while some mention an inversion of the 2Y/10Y leaves us on average more than a year and half to face a potential recession, it is worth highlighting that a recession occurring after a 1st rate hike in a cycle happens earlier when the 2Y/10Y inversion occurs during the hiking cycle. The last inversion of March 2022 occurred in the quickest time span recorded after the start of the hiking cycle.

US 3M/10Y vs 2Y/10Y:

Asset class performance post-inversion

The average performance post inversion of the S&P 500 does not show cast a clear pattern. No correlation can be established between the inversion and performance of US stock index before, during and after a cycle.

We should bear in mind that short and long-term dynamics shape the yield curve. Two years ago, before the COVID-19 outbreak the FED has cut its policy rate to near zero in order to limit the impact of a recession caused by the pandemic.

Fast forward to today’s terms, the FED has to “catch up” with growing inflation as both global and US economy recovers to its pre-pandemic levels. The T-Bill is facing strong global demand combined to the FEDs’ ongoing quantitative easing (QE) that has for effect to increase prices of bonds resulting in low yields. The steepness of short-term yields has caught a great deal of attention, ultimately opening the debate of future economic outlook on either an unconventional slowdown in growth or a strong signal of a US recession; the question remains open.

Mehr Publikationen

05.08.2026

Wird die Kernenergie die Energiequelle für die KI-Revolution sein?

Die Kernenergie entwickelt sich aufgrund ihrer Fähigkeit, stabilen, grossvolumigen und kohlenstoffarmen Strom bereitzustellen, zu einem der führenden Kandidaten für die Energieversorgung der KI-Revolution.

Mehr dazu01.08.2026

Einen schönen Schweizer Nationalfeiertag!

Heute feiern wir nicht nur einen Nationalfeiertag, sondern auch die Werte, die die Schweiz seit Generationen prägen: Vertrauen, Zuverlässigkeit und Spitzenleistungen.

Bei Cité Gestion sind diese Grundsätze Teil unseres Erbes und bilden die Grundlage für unser tägliches Engagement.

24.07.2026

Was wäre, wenn Deutschland endlich aufwachen würde?

Deutschland bereits 2027 wieder zum Wirtschaftsmotor Europas werden.

Mehr dazu07.07.2026

Willkommen, Vincent Lecoultre!

Wir freuen uns, Ihnen mitteilen zu können, dass Vincent Lecoultre als Banker zu Cité Gestion gekommen ist.

Mehr dazu30.06.2026

Warum könnte der Rückgang der Ölpreise die Investitionslandschaft in den kommenden Monaten neu gestalten?

Niedrigere Ölpreise könnten die Investitionsaussichten in vielerlei Hinsicht verändern.

Mehr dazu23.06.2026

Reitturnier von Crête x Cité Gestion

Wir sind stolz darauf, das Reitturnier auf Kreta unterstützt zu haben – eine aussergewöhnliche Veranstaltung, die Leidenschaft, Spitzenleistungen und Geselligkeit vereint und dabei Werte verkörpert, die uns am Herzen liegen.

Mehr dazu