09.10.2020

Quel est le prix du risque à l'approche des élections américaines ?

There is no doubt that a US presidential election represents a risk for financial markets and a good way to quantify how much risk is currently priced-in is to look at the forward implied volatility before and after the elections.

For that, the VIX index, a basket of the S&P 500 options volatility, sounds a good barometer.

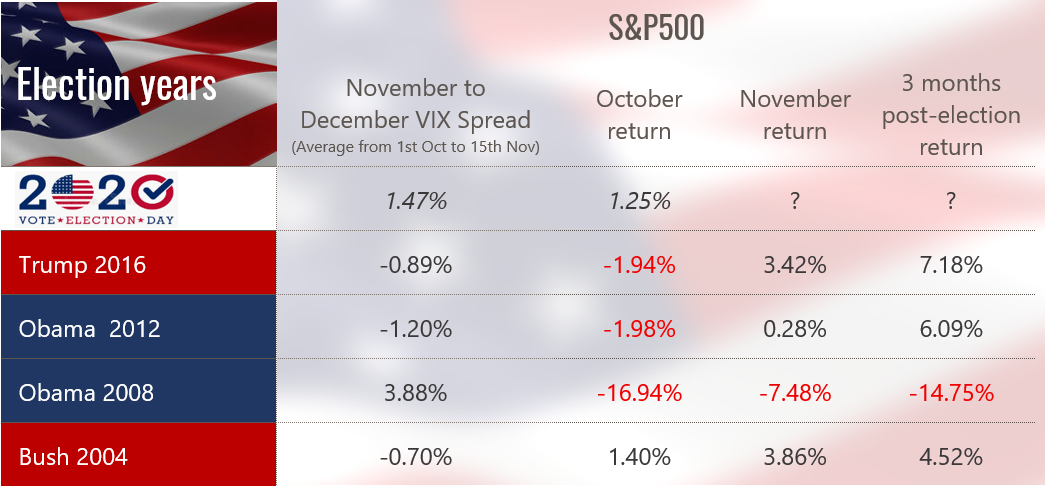

Looking at the VIX curve, The November expiry is currently trading 1.5% above the December one, reflecting the immediate risk investors are facing post-election (November 3rd) relative to December.

While the 1.5% spread indicates a higher implied risk around and after the election, it does not quantify the absolute level of risk. To put it in perspective, we looked at the average November-December VIX Spread from October 1st to November 15th for every US Election since 2004.

Excluding the US election during the Great Financial Crisis in 2008 where spot volatility was structurally higher than 1, 2 and 3 months forward, it appears that a positive November/December VIX Spread is somewhat unusual. In fact, during the 2004, 2012 and 2016 elections, the November VIX never traded above the December one.

Looking at the return of the S&P in October, November and 3 months after the election, we can observe that it is very difficult to draw any conclusion over a US presidential election from a financial market perspective. If anything and excluding the 2008 election during the crisis, the simple and most direct conclusion would be that a US presidential election after 2000 had a positive impact on the S&P 500 Index one month and 3 months after the outcome.

So how to explain this extra-risk this time? We believe the 1.5% premium in November volatility relative to December likely reflects one single risk: if Biden wins, President Trump might not going to accept it. A sentiment that has been reinforced after the first TV debate of the US elections.

To conclude, history shows that financial markets can easily deal with a republican or democrat president but definitely not with no President after November 4th.

Autres publications

05.08.2026

L'énergie nucléaire sera-t-elle la source d'énergie de la révolution de l'IA ?

L'énergie nucléaire s'impose comme l'un des principaux candidats pour alimenter la révolution de l'IA, grâce à sa capacité à fournir une électricité stable, à grande échelle et à faible empreinte carbone.

Lire plus01.08.2026

Joyeuse Fête nationale suisse !

Aujourd’hui, nous célébrons non seulement une fête nationale, mais aussi les valeurs qui façonnent la Suisse depuis des générations : la confiance, la fiabilité et l’excellence.

Chez Cité Gestion, ces principes font partie de notre héritage et constituent le fondement de notre engagement au quotidien.

24.07.2026

Et si l'Allemagne était enfin en train de se réveiller ?

Si Berlin concrétise enfin ses promesses, l'Allemagne pourrait redevenir le moteur économique de l'Europe dès 2027.

Lire plus07.07.2026

Bienvenue à Vincent Lecoultre !

Nous avons le plaisir d’annoncer l’arrivée de Vincent Lecoultre en tant que banquier chez Cité Gestion.

Lire plus30.06.2026

Pourquoi la baisse des cours du pétrole pourrait-elle bouleverser le paysage de l'investissement au cours des prochains mois ?

La baisse des cours du pétrole pourrait modifier les perspectives d'investissement de multiples façons.

Lire plus23.06.2026

Concours Hippique de Crête x Cité Gestion

Nous sommes fiers d'avoir soutenu le Concours Hippique de Crête, un événement d'exception qui réunit passion, excellence et convivialité autour de valeurs qui nous sont chères.

Lire plus